Your Assets are At Risk.

Let’s protect it!

We have analyzed hundreds of Supreme Court cases. Whether you need to protect assets from lawsuits, creditors, Medicaid, or divorce, or want peace of mind and optimized taxes, we’ve got you covered with a customized plan.

Your confidentiality is our top priority. We use advanced technologies and strict protocols to ensure your information remains secure. We understand the importance of discretion for high-net-worth individuals, and our tailored strategies guarantee that your assets are protected with the highest level of confidentiality.

We stay ahead of potential threats with proactive risk management. Our top asset protection lawyers regularly attempt to breach our own trusts to identify and fill any gaps. Combined with our exceptional customer service, we continuously update your asset protection plan to address emerging risks and evolving needs, ensuring your wealth remains secure and your experience seamless.

The System Isn’t Broken.

It’s Feeding Off You - Exactly As Designed. You’ve been told the system is here to protect you. That the courts are fair. That your will or trust is “enough.” That if you follow the rules, your family will be okay.But here’s the truth:The system wasn’t built to protect you. It was built to extract from you.

Let’s break it down:

Probate courts charge fees on your estate, sometimes 7% or more, just to “process” what should’ve gone straight to your family.

Lawyers bill hundreds per hour while dragging your case out for months.

The IRS waits until you die, then takes a second cut from your after-tax assets.

Lawsuits don’t need to win. They just need to scare you long enough to settle.

Need Your Trust Reviewed?

Let Our Experts Customize your Trust Template

for Unshakeable Peace of Mind.

You’ll Discover:

Why most “standard” trusts collapse in court and what makes this one different

How to stay in full control while making your assets legally unreachable

A checklist showing what to do today to secure your future

How to pass your home, savings, or business to your family without probate

The best states for maximum protection

Why the government hates this setup but can’t stop it

The real reason wills don’t protect you and what actually does

You've taken the crucial first step. You've armed yourself with the Bulletproof Trust Templates.

But as you dive in, a silent, persistent question often emerges in the back of your mind, a concern that keeps even the most diligent individuals awake at night:

"Am I doing this right? Is my trust truly bulletproof, or could a hidden flaw, a forgotten detail, or an unforeseen legal shift leave my family and legacy vulnerable?" It’s more than a valid concern; it’s the stark reality facing anyone striving for genuine, ironclad asset protection. Crafting a plan that truly stands the test of time, and the unpredictable nature of life, demands precision, foresight, and an intimate understanding of legal nuances that shift like quicksand. Without expert oversight, even with the finest blueprints in your hands, the slightest miscalculation – a forgotten signature, an outdated clause, or an improper asset transfer – can bring the whole protective structure crashing down. This is when your meticulously built legacy – your hard earned assets, your family's financial security, everything you’ve diligently built, becomes an open target for opportunistic lawsuits, draining probate battles, unexpected divorces, or relentless IRS audits. The moment of truth, unfortunately, often comes when it's already too late to fix. But what if you could finally eliminate that uncertainty? What if you could gain absolute clarity and ultimate protection, without the exorbitant fees or the constant worry that a single mistake could unravel everything? That's precisely why we're here to offer you unparalleled, personalized guidance.

Imagine this: Direct, one-on-one access to seasoned legal minds who can personally review your trust documents and meticulously customize your trust templates. This isn't about generic advice; it's about tailoring every aspect to your unique family situation, your specific goals, and the ever-evolving legal landscape. Our professional, licensed lawyers will work with you, answering every question and confirming every critical step, ensuring your plan is as robust as it can possibly be.

Beyond just handing you templates, we’ll actively review your trust documents to ensure they are ironclad and perfectly aligned with your goals:

We will personally review your trust documents (unlimited times) fixing errors, updating language, and tailoring them to your unique family and financial situation.

We will analyze tax consequences tied to your trust, helping you avoid costly mistakes and making sure your structure minimizes exposure.

We will confirm every critical detail is correct,from asset transfers to legal clauses, so nothing is left vulnerable.

We will act as a second set of expert eyeseven if you already hired another attorney, our team will catch loopholes or oversights others miss.

All reviews are customized specifically for you, with every question answered by our licensed legal professionals.

This is the kind of bespoke legal expertise that normally comes with a price tag upwards of $500 an hour. But today, and only on this page, we're offering you this comprehensive, personalized guidance at an unprecedented value.

What's Holding You Back from Absolute Peace of Mind?

You've tried to secure your future, but have you ever felt that nagging doubt? The real problem isn't a lack of desire to protect your family; it's the fear of making a critical error in a complex legal landscape.

Most people struggle because they're navigating these intricate waters without a seasoned captain, hoping templates alone will suffice. They may have even invested in other solutions, only to find themselves still asking, "Is this truly secure?" It's not your fault if previous attempts haven't given you 100% confidence. The legal world is designed to be complex, and without expert guidance, it's easy to miss the hidden pitfalls.

But what if you could finally eliminate that uncertainty? What if you could have true clarity and ultimate protection, without the exorbitant fees or the constant worry?

Your "Done-With-You" Personal Legal Strategist

For years, this level of direct, personalized access to our asset protection attorneys was reserved exclusively for our ultra-high-net-worth private clients — those who pay upwards of $30,000 for bespoke legal services and ongoing counsel.

We’ve never before made this available to the public. It was the "secret weapon" for clients who demanded absolute certainty and peace of mind, knowing every detail was flawless.

But here’s the game-changer…

The single biggest roadblock to truly bulletproofing your assets isn't a lack of information; it's the fear of getting it wrong, or not having direct access to an expert who can clarify your unique situation. We know you have specific questions, complex family dynamics, and concerns that no pre-written template can fully address.

So today, just on this page and just as a one-time offer, you can unlock immediate access to our top trust attorney.

Right here, right now, you can gain the confidence that comes from having a seasoned legal mind overseeing your asset protection. Skip the exorbitant hourly fees, eliminate the guesswork, and finally ensure your wealth is bulletproofed – with every question answered and every critical step confirmed by an expert.

This personalized guidance is your ideal solution if you demand absolute certainty for your assets, if you have specific legacy planning needs, or if you simply refuse to leave your family's financial future to chance.

When you experience the profound peace of mind knowing you have a dedicated legal expert by your side, ensuring every aspect of your trust is perfect, you'll understand why this is the ultimate "bulletproof safety net" for your entire life.

Our private mentorship clients gladly pay over $30,000 for this exact personalized guidance and ongoing support. This direct legal oversight was the cornerstone of that exclusive program.

And the blunt truth is - with just one unforeseen lawsuit, one unexpected divorce, or one critical audit… this personalized guidance could save you 10-20 times over what you invest today.

Because you’re getting everything you need to set up and maintain your Bulletproof Trust with ongoing, personalized legal oversight from an expert, without paying $30,000+ in hourly legal fees, this program would easily be valued at $4,997.

But today you won't be paying that.

Today as a part of this one time offer,

you can get ongoing trust document reviews, unlimited Q&A, and access to a private community of peers actively building their own Bulletproof Trusts for incredibly low investment of $2,499:

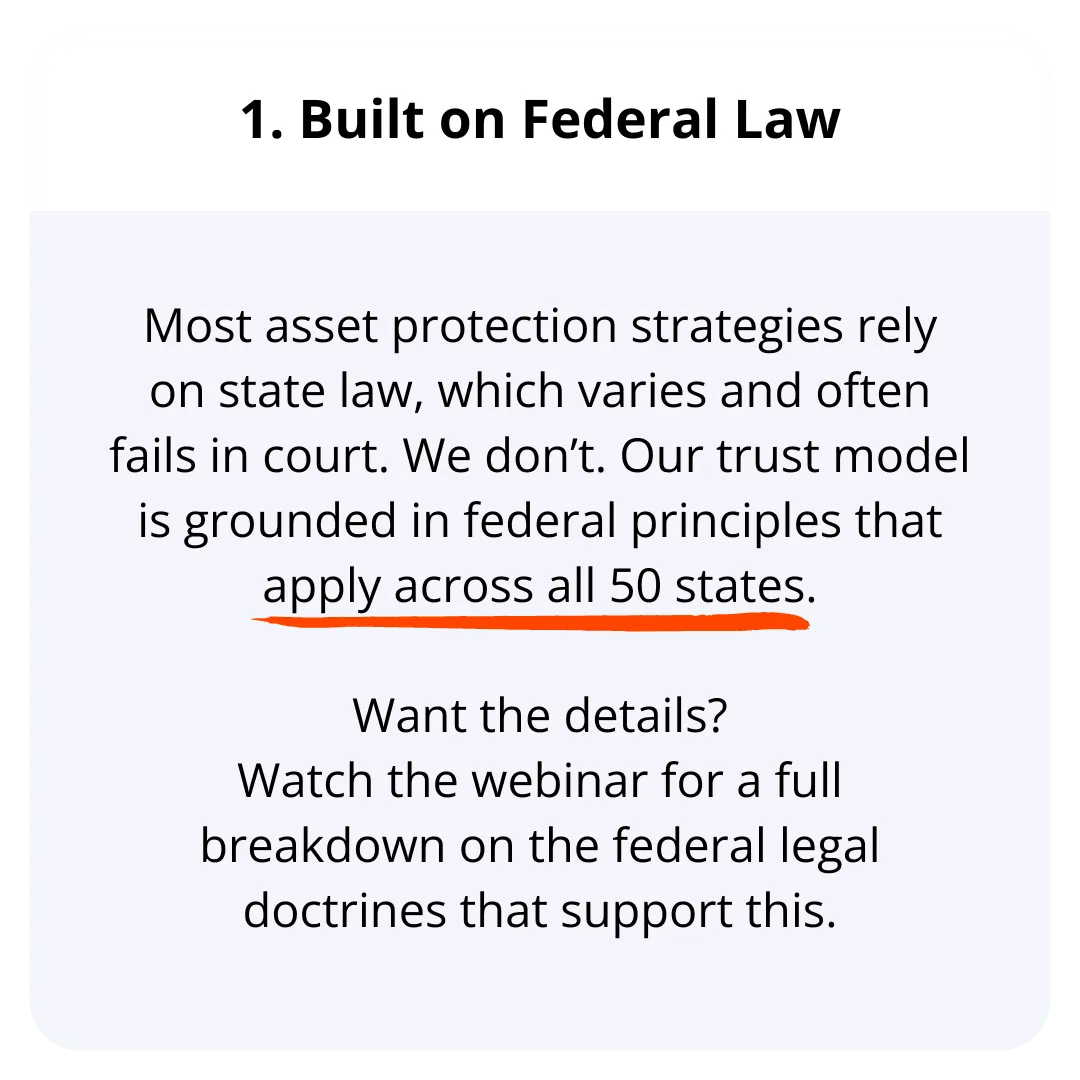

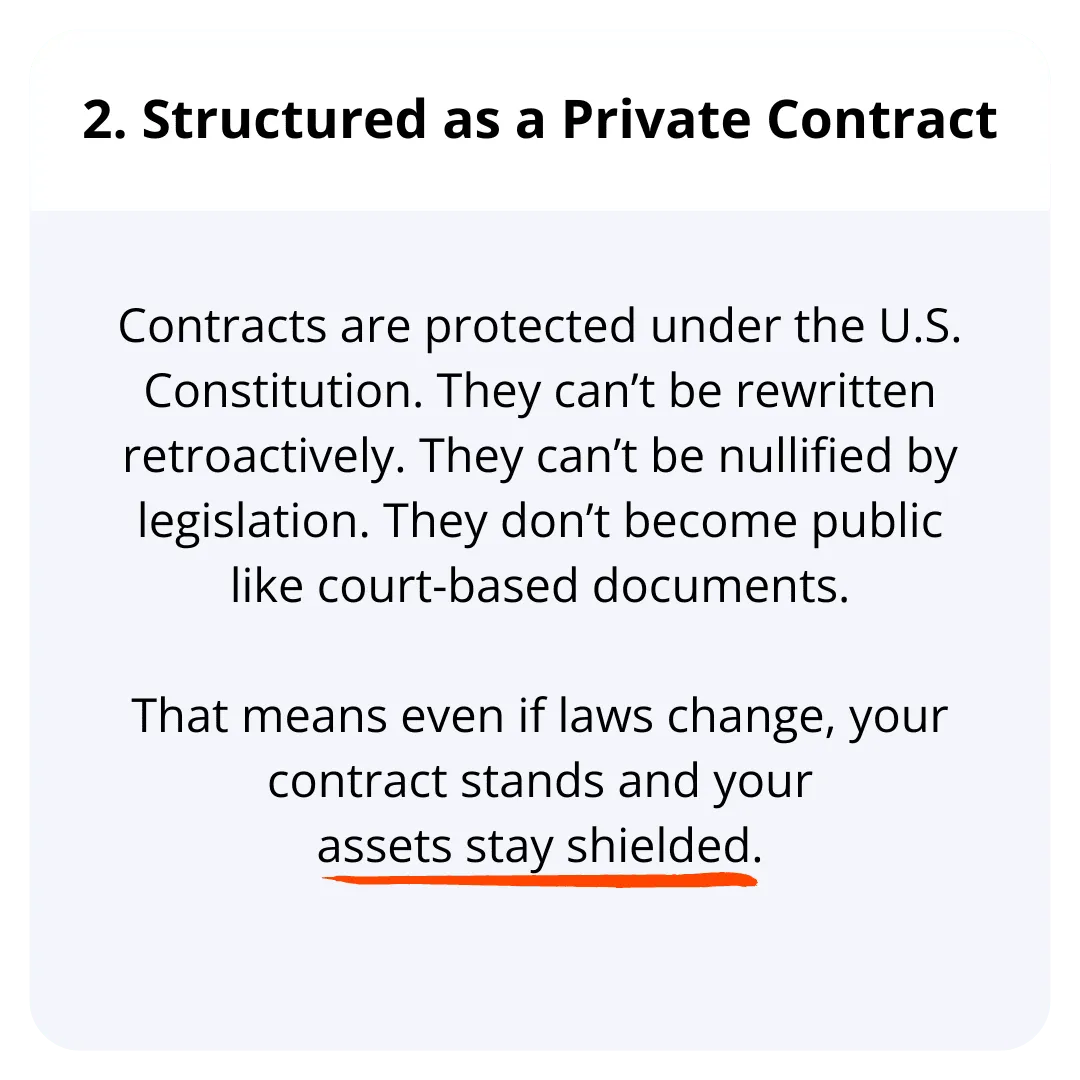

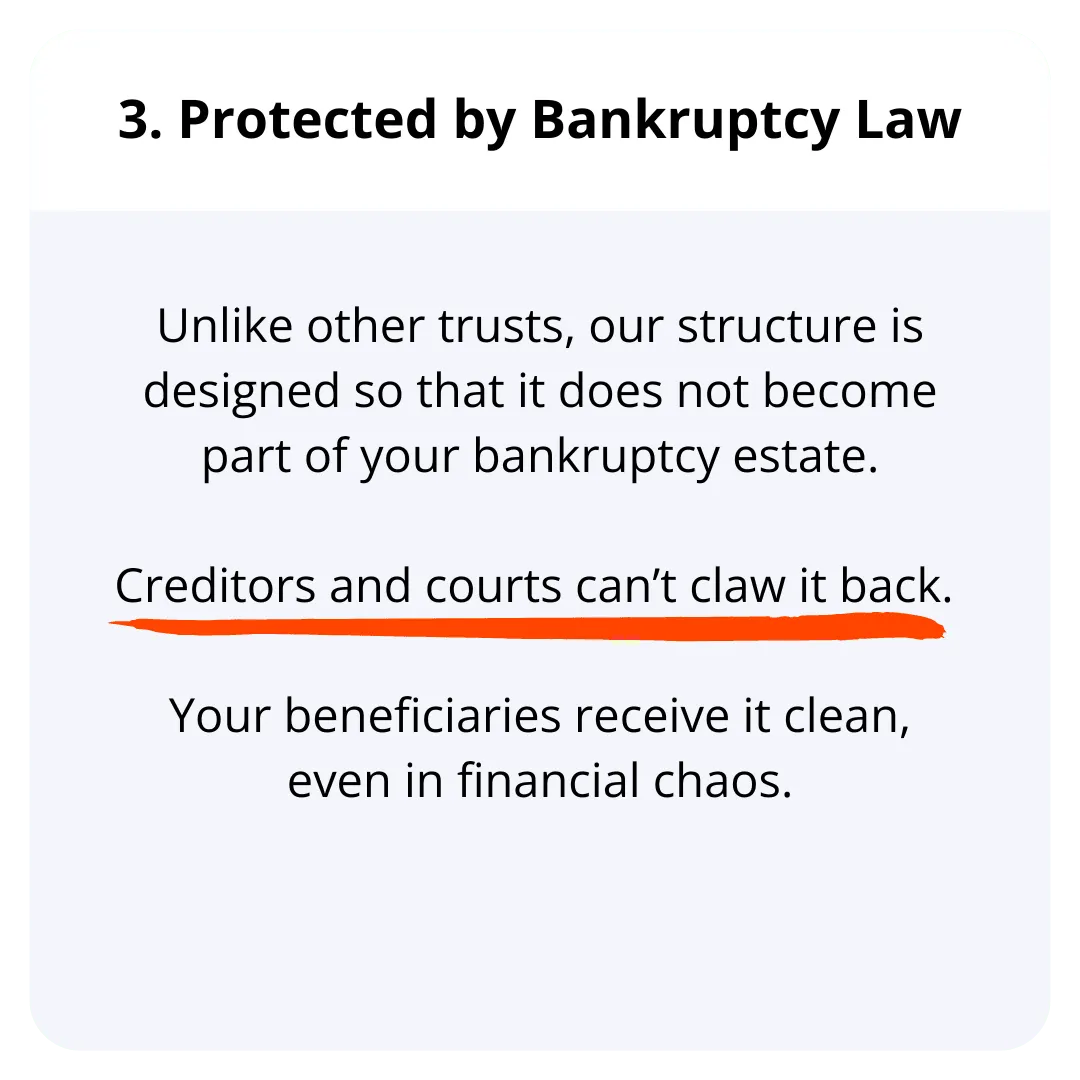

You’ve heard of trusts. You may even have one.

But what you haven’t seen until now, is a trust structure that combines federal legal force, contractual shielding, and bankruptcy immunity into one.

Here’s what makes the Bulletproof Trust strategy uniquely effective:

Your Bulletproof Trust includes:

Secret Guide #1: The Trust Tax Handbook ($297 Value)

The "3-Layer Tax Shield" that saved one client $127,000 in capital gains

How to legally shift income between tax years

The "Nevada Incomplete Gift" strategy billionaires use

Warning: 7 trust moves that trigger immediate IRS audits

The "Charitable Remainder Hack" that creates tax-free income

Secret Guide #2: Trust Law Mastery Guide ($197 Value)

The 17 legal attacks that break 93% of trusts (and how to block each one)

State-by-state trust law comparison chart

"Magic words" that make your trust legally bulletproof

The #1 mistake that voids spendthrift protection

How to legally move your trust to save thousands

Secret Guide #3: Trust Web Navigator ($97 Value)

Interactive flowchart: "Which trust type saves you the most?"

State trust law calculator (find your optimal jurisdiction)

Tax savings estimator tool

Legal document audit checklist

Monthly trust law updates (laws change fast!)

Second Set of Eyes (Even If You Already Hired a Lawyer): Even if you’ve already worked with another attorney, our team will catch hidden flaws or oversights others might miss, ensuring your plan is bulletproof.

Tax Consequence Reviews: Every trust decision carries potential tax exposure. Our professionals will review your trust structure and help you understand the tax consequences so you don’t face unexpected bills.

Direct Answers to Your Questions: Ask our legal team anything about your trust, family situation, business holdings, or real estate. Get clear, expert guidance without guesswork.

Unlimited Trust Reviews by Real Attorneys: Our licensed asset protection lawyers will personally review your trust documents as many times as needed: fixing errors, updating language, and tailoring everything for your specific life.

You will finally have crystal clear clarity and ultimate protection for:

How to perfectly tailor your trust for your unique family situation with expert oversight and personalized advice.

How to ensure every asset is correctly transferred and truly locked away from threats, with a lawyer confirming each step.

That your family is fully protected (even if you get hit by a bus tomorrow) because you have a legal expert ensuring everything is perfectly aligned with your goals.

COMPANY

LEGAL

CONTACT US

©Copyright 2025. WealthTaxAdvisor.net All Rights Reserved.